Highlights of FAQ issued by CBDT on Vivad Se Vishwas

Vivad se Vishwas scheme is a scheme introduced, in order to reduce the number of pending Income tax Litigations, to ease the life for taxpayers and at the same time to increase the revenue for the Government.

To get the most out of the scheme, one must have a clear picture of what the scheme is offering. In order to clear the queries of the taxpayers, CBDT has released the first list of FAQs. Some of the key clarifications have been illustrated below

Clarification of Appeals Eligible under VSV

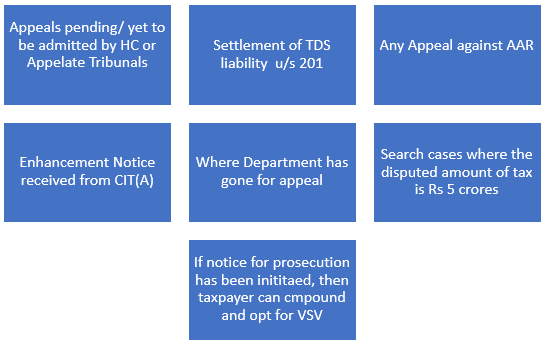

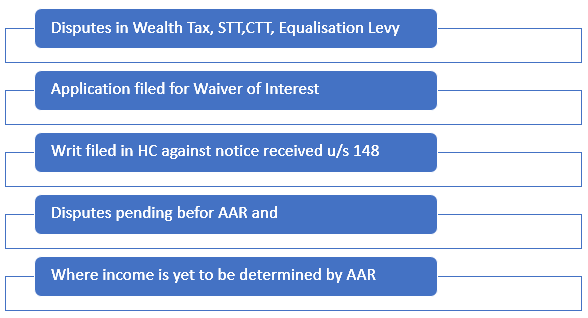

Clarification of Appeals Ineligible under VSV

Withdrawal of Appeal

1. By the Assessee

2. By the Department

Upon intimation of appellant, the payment of tax to the DA, the Department shall withdraw the appeal

Other Key Clarifications

1. For each assessment, year, one declaration will have to be filed. If we have dispute in 3 AY, then we will have to file 3 declarations

2. Even if there is no demand for Interest u/s 220, appellant should file a declaration for the waiver of the same

3. If the dispute is for both the tax and penalty, then appellant must file declaration for both, but must pay only the amount of disputed tax

4. We must opt the scheme for all pending issues with respect to particular order and we cannot select any issues optionally

5. DA shall not institute any further proceedings with respect to the tax arrears

6. If there are multiple assessments for a particular year, then the assessee can either settle all the pending assessments or select any of the assessments.

7. Tax and Fee (234E and 234F) must be settled separately

8. If any rectification order is pending from AO, then the disputed tax amount shall be calculated after taking to consideration rectification.

9. No interest for the excess tax deposited under VSV Scheme

10. The order of the DA cannot be appealed

With the first set of 55 FAQ, many of the queries of the taxpayers would have resolved and we may expect further clarifications from the Department so that the taxpayers and as well as the Department get the most out of it, by also reducing the number of pending litigations.

Disclaimer:“The information contained herein is only for informational purpose and should not be considered for any particular instance or individual or entity. We have obtained information from publicly available sources, there can be no guarantee that such information is accurate as of the date it is received or it will continue to be accurate in future. No one should act on such information without obtaining professional advice after thorough examination of particular situation.”

Prepared By

Srivatsa Jois H S

CA Final

Date: 10/04/2020